Simulations Plus (SLP) Sophon Profile

An emerging leader in bio-simulation software, flying under the radar

Since launch, our goal with Sophon Microcap Atlas has been to build the definitive research hub for underfollowed sub-$500M companies. Each month we’re adding deep-dive coverage, proprietary scoring frameworks, and differentiated insights you won’t find anywhere else. With every report, the value of the platform compounds — but so does the subscription price.

We’ve structured it this way deliberately: to reward early adopters who believe in what we’re building. Subscribers who joined at launch are still paying their original rate, and they’ll keep that price for life. By contrast, new readers coming in today are already paying more than they did six months ago.

That’s by design. We’re investing heavily in research, and we want to keep the economics aligned with our most loyal readers.

When you join Sophon Microcap Atlas, your subscription price is locked in for life. We raise rates by $15 every two months to reflect the growing value of our research library, but early subscribers keep their lower rate forever. On November 1, the price rises to $60/month or $540/year — lock in now at $45/month or $400/year and you’ll still be paying that rate years from now, even when the service is worth thousands.

Disclaimer: Not financial advice

View: Pass

Sophon Score: 66/100

We will not pursue Simulations Plus as an investment or include it in coverage because the core opportunity, while defensible, is relatively small and niche.

Recent execution missteps, including impairments from acquisitions and services volatility, highlight operational risk that could continue to weigh on margins. Growth is partially tied to biotech cycles, making the revenue stream less predictable despite sticky software renewals. Competitive pressure from larger, bundled players like Certara limits upside.

While the balance sheet is solid and regulatory credibility is strong, the combination of scale constraints, execution risk, and cyclicality makes it unattractive relative to other opportunities in our coverage universe.

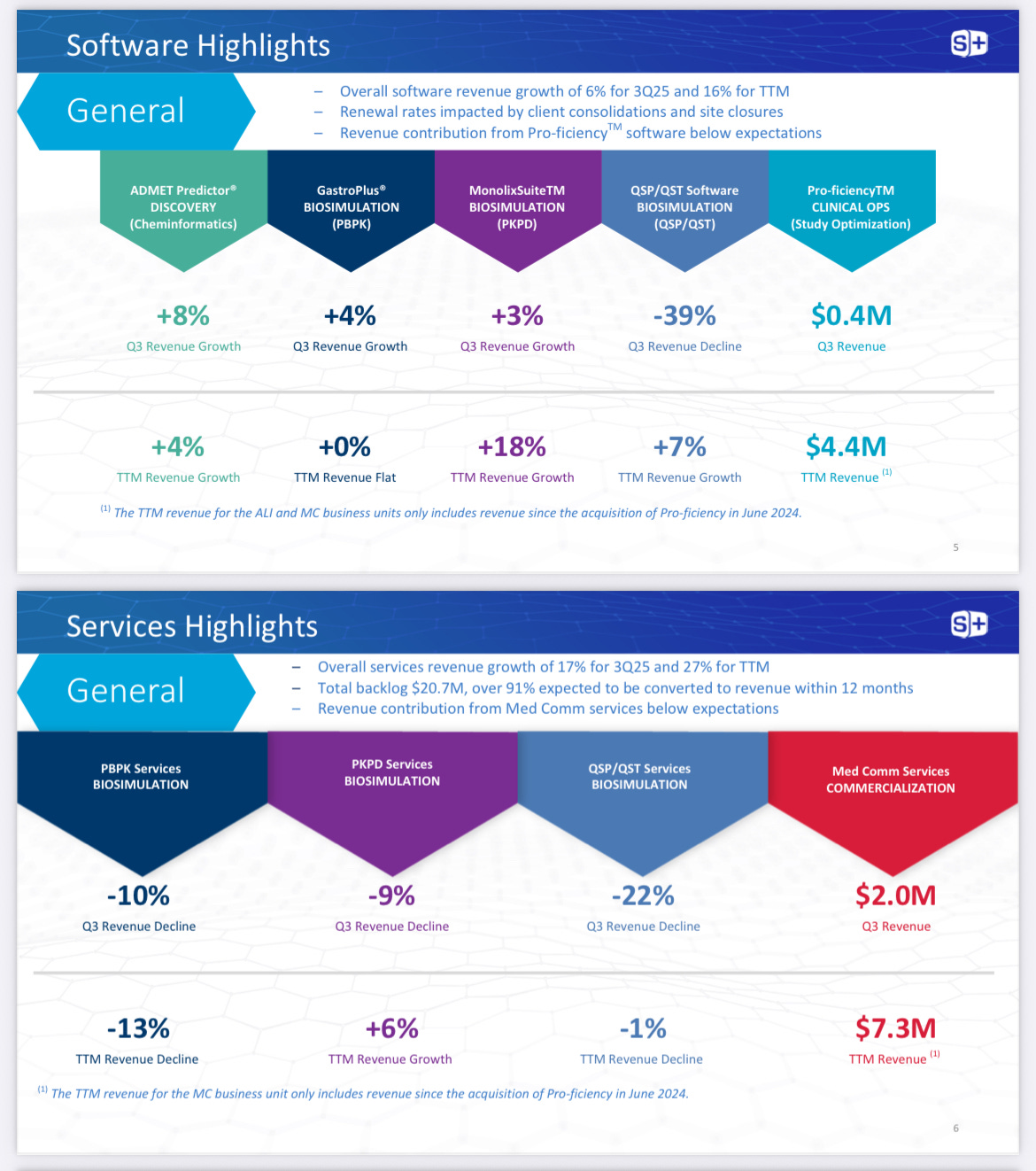

Simulations Plus plays in a niche market: software that helps drug companies simulate how a medicine will behave in the body before running full-scale lab or clinical trials. The core market for this “biosimulation” software is `$4B today, growing LDD over time. Mgmt argues the oppt’y is closer to $8B if you include their new push into training and medical communications, but that’s still small compared to the broader clinical trial industry.

In practice, that $8B TAM view reflects the addition of Pro‑ficiency’s adaptive learning (training) and medical communications units (now ALI and MC) to Simulations Plus’ product suite, which complement the core tools GastroPlus (PBPK), MonolixSuite (PK/PD), and ADMET Predictor (AI/ML‑based discovery). Independent industry trackers still peg the pure biosimulation market at only a few billion dollars but note mid‑teens growth in prior years decelerating toward ~10% as the category matures.

Keep reading with a 7-day free trial

Subscribe to Sophon Microcap Atlas to keep reading this post and get 7 days of free access to the full post archives.