SmartCraft ASA (SMCRT.OL) Initiating Coverage

Norwegian SaaS company providing sticky, mission-critical software in one of Europe’s least digitized industries

Since launch, our goal with Sophon Microcap Atlas has been to build the definitive research hub for underfollowed sub-$500M companies. Each month we’re adding deep-dive coverage, proprietary scoring frameworks, and differentiated insights you won’t find anywhere else. With every report, the value of the platform compounds — but so does the subscription price.

We’ve structured it this way deliberately: to reward early adopters who believe in what we’re building. Subscribers who joined at launch are still paying their original rate, and they’ll keep that price for life. By contrast, new readers coming in today are already paying more than they did six months ago.

That’s by design. We’re investing heavily in research, and we want to keep the economics aligned with our most loyal readers.

When you join Sophon Microcap Atlas, your subscription price is locked in for life. We raise rates by $15 every two months to reflect the growing value of our research library, but early subscribers keep their lower rate forever. On November 1, the price rises to $60/month or $540/year — lock in now at $45/month or $400/year and you’ll still be paying that rate years from now, even when the service is worth thousands.

View: Buy

Sophon Score: 81/100 (see evaluation rubric at end of note)

SmartCraft is well positioned in one of Europe’s least digitalized industries, with sticky, mission-critical software that helps small contractors improve profitability across people, materials, and compliance. Its recurring revenue base is strong, churn is mainly tied to bankruptcies rather than competition, and the U.K. offers a long runway for expansion.

Construction remains one of the least digitalized industries in Europe.

Many small and mid-sized contractors — electricians, plumbers, and general trades — still manage their businesses on Excel or even pen and paper. SmartCraft is targeting this gap, offering software that moves these companies off manual processes and into integrated, cloud-based workflows.

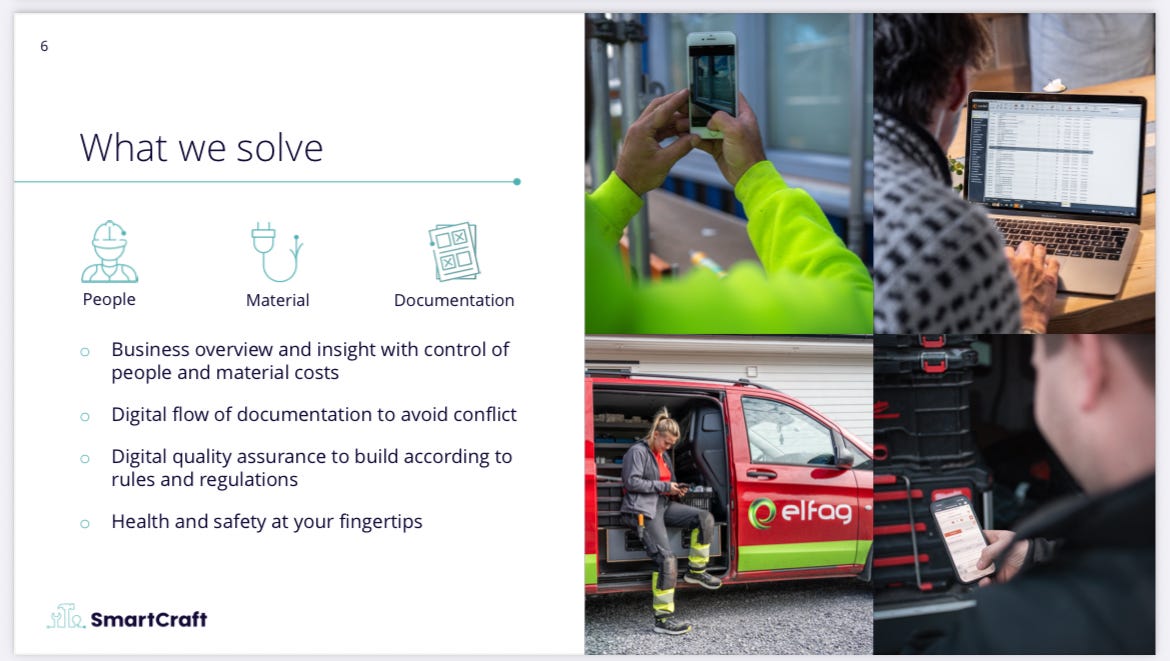

For its customers, SmartCraft is more than an efficiency tool. It touches the three core levers of profitability — people, materials, and documentation.

People: Scheduling, time tracking, and field reporting.

Materials: Procurement, cost control, and waste reduction.

Documentation: Compliance, safety, and project records, including emerging ESG requirements.

By capturing these workflows in one system, SmartCraft helps contractors invoice more jobs, price accurately, and avoid costly errors. For SMEs that operate on thin margins, the software quickly becomes mission-critical.

Customers adopt SmartCraft where the impact is most tangible:

Invoicing ensures every job gets billed, including small service calls that are often missed.

Quoting and Calculation tools give electricians and plumbers fast, accurate estimates to win business without underpricing.

Documentation and Compliance modules meet growing regulatory demands and create stickiness.

Project Management tools like Bygglet and Cordel keep jobs on track.

People and Materials Management replace spreadsheets and manual processes.

The key opportunity: roughly half the target market still runs on outdated tools, leaving a large base to digitalize.

SmartCraft’s software is embedded in daily operations, which creates natural stickiness. Customers rarely churn to competitors; the main source of attrition is bankruptcies among small contractors. Larger firms typically downgrade (reduce seats or features) rather than cancel, underscoring the platform’s necessity.

Management is layering on adjacencies to increase wallet share:

Building a full electrician ecosystem by consolidating solutions and adding quoting and calculation tools.

Launching Tellus, an open-source platform for emissions tracking, to address ESG requirements.

Rolling out a long-awaited budgeting module.

Expanding APIs and integrations with accounting software and distributors.

Experimenting with AI to improve onboarding and customer support.

Entering the UK market through acquisitions and adaptation of Nordic solutions.

Each initiative is designed to expand ARPU through upsell and cross-sell opportunities.

SmartCraft serves ~13,800 customers and ~120,000 users, primarily SMEs focused on maintenance, renovation, and service work — a segment that is larger and less cyclical than new construction. Electricians and plumbers make up the majority of users. The company operates mainly in the Nordics, with the UK now representing its largest near-term expansion opportunity.

Organic ARR growth comes from both new customer acquisition and expansion within the base. In some quarters, new logos account for 70% of growth; in others, the split is closer to even. Upsell remains underdeveloped but is a key lever going forward.

SmartCraft is not competing head-on with large ERP vendors. Instead, it is consolidating the fragmented, under-digitalized SME segment of construction. For these businesses, SmartCraft is not optional software — it is a profit enabler that replaces outdated, manual processes. That positioning creates both resilience in downturns and meaningful upside as the industry catches up in digital adoption.

SmartCraft holds a leading position in the Nordics, with Norway and Sweden contributing roughly 88% of revenue. Both markets are driven by SMEs focused on renovation, upgrades, and services, and both continue to deliver solid organic growth (Norway +13% YoY in Q1 2024, Sweden +14% in Q1 2024 and +11% in Q3 2024). Sweden is anchored by Bygglet, the company’s largest solution by revenue.

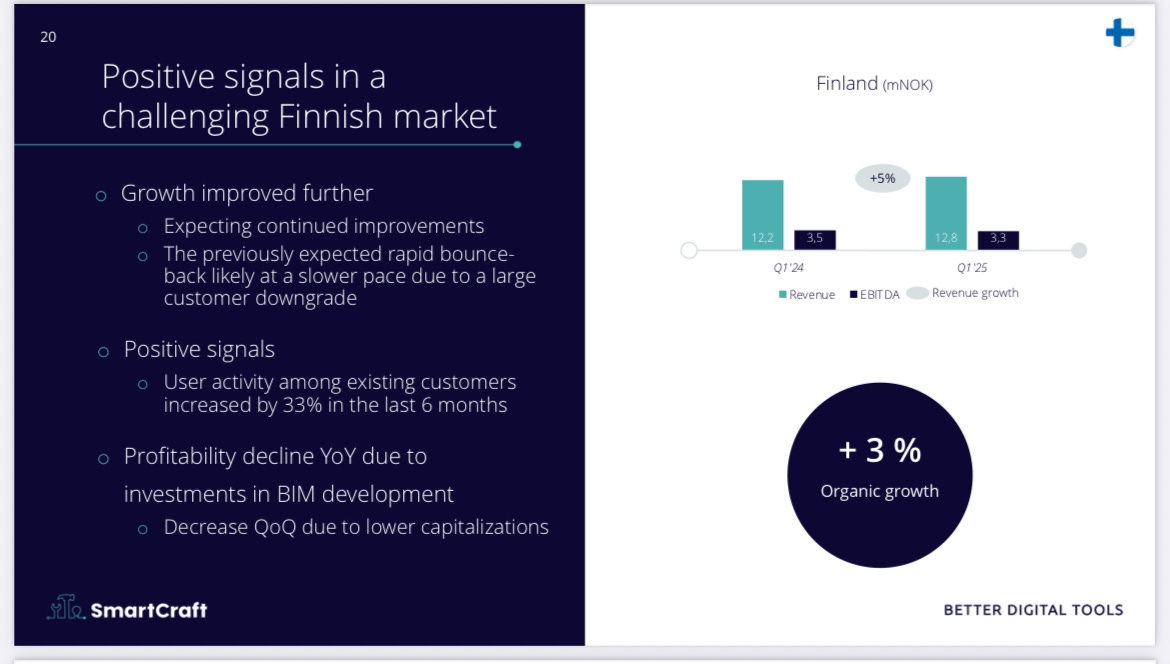

Finland has been weaker. The business there historically skewed toward larger enterprises and new-build projects, a segment hit hard by macro headwinds. Recurring revenue growth was negative (-5% in Q1 2025), though SmartCraft is repositioning around SMEs with solutions like EL-VIS.

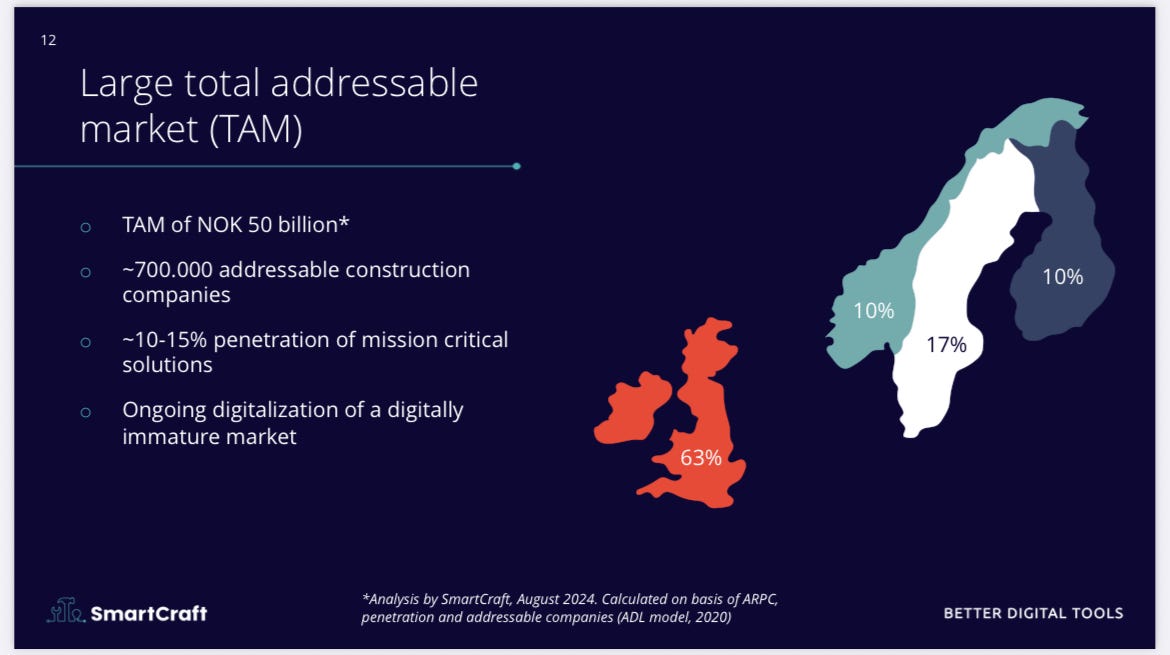

The addressable market is substantial. SmartCraft estimates NOK 50 billion across the Nordics and U.K., representing ~700,000 firms, with digital penetration still only 10–15%. The U.K. alone now represents 60%+ of TAM following the Clixifix acquisition.

Structural tailwinds are strong:

Construction remains one of the least digitalized industries, with ~40–55% of workers still using pen-and-paper or spreadsheets.

Energy efficiency mandates are driving demand for electricians and plumbers — SmartCraft’s core users — who are already capacity constrained.

Compliance and documentation requirements are expanding, including materials declarations, HSE reporting, and emissions tracking. SmartCraft’s Tellus solution is designed to meet these demands.

Renovation and maintenance — a less cyclical and larger segment than new construction — is SmartCraft’s main customer base.

The construction industry faces structural challenges that naturally drive demand for SmartCraft’s offering (see slide below)

Competition is highly fragmented, mostly local point solutions with limited scale. SmartCraft has positioned itself as a consolidator. Some competitors have been acquired (e.g., EQT buying two Swedish firms), but many smaller players have scaled back. Larger international SaaS names like Procore and Autodesk are present but focus on enterprises; SmartCraft’s niche is SME-specialized workflows and integrations with ERP/accounting systems like Visma.

The U.K. is the key expansion market. Clixifix provides a beachhead, and management believes Nordic solutions can be adapted to a market they view as less digitally mature. Marketing has scaled efficiently, with 5x brand exposure YoY in Q2 2024, a centralized sales engine, and growing inbound demand.

Recurring revenue dominates, consistently 93–96% of the mix. In Q2 2025, it was 95.5%. SmartCraft deliberately converts one-time services into subscriptions, often at the expense of short-term revenue and EBITDA, to ensure predictability and stickiness.

Margins reflect SaaS-like economics, though diluted by acquisitions. Adjusted EBITDA margin was 37.2% in 2024 (41.6% in 2023) and 38.2% in Q2 2025. Adjusted EBITDA–CapEx margin was 27.7% in 2024. Acquired firms often start with little to no margin, but SmartCraft has a track record of lifting profitability over time. Management expects margins to trend higher as scale improves.

Customer economics are attractive. LTV/CAC was 18x in the first half of 2023 (previously >20x). Sales efficiency is supported by automation and online channels: in Q4 2023, 28% of new customers came via online sales, up from 21% a year earlier. Marketing spend has driven sharp increases in leads and brand awareness without a comparable rise in costs.

Churn is concentrated in small customers, often due to bankruptcy, while larger firms tend to downgrade rather than cancel. Contribution margins per customer are described as strong, though not disclosed in detail.

SmartCraft combines organic growth with steady M&A. In 2024, total revenue grew 27% (8% organic), while ARR grew 25% (8% organic). Q1 2025 saw +23% ARR YoY (+6% organic). Since IPO, CAGR has been 27%. The company targets 15–20% medium-term organic growth.

The M&A playbook is repeatable: acquire complementary SaaS with ARR growth, recurring-heavy revenue, and low churn; integrate them onto SmartCraft’s tech stack; convert one-off sales to recurring; and expand margins. Twelve acquisitions have been completed since 2017, including 10 in the last five years, with a strong pipeline in place — especially in the U.K.

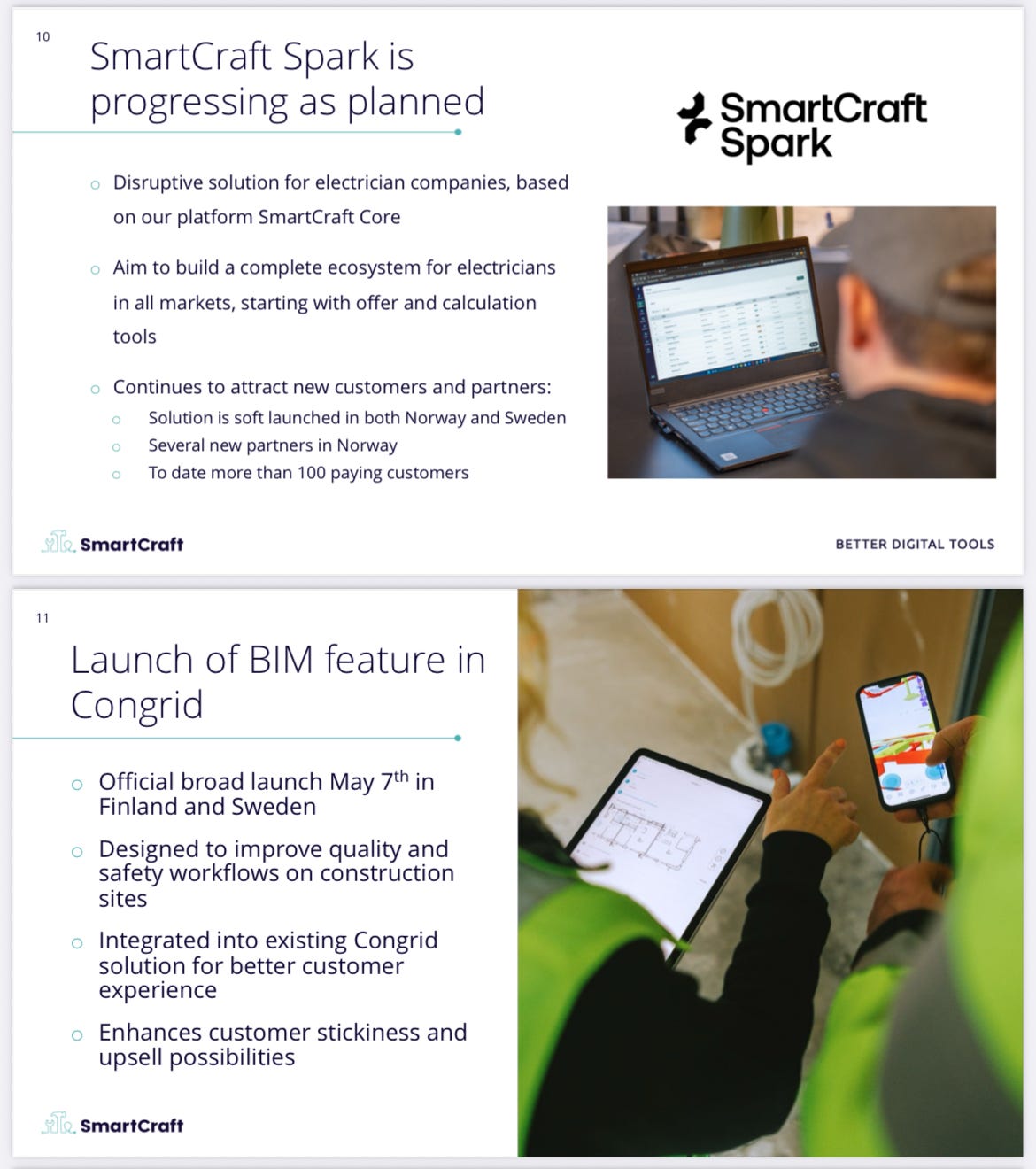

Cross-sell is underexploited but viewed as a large ARPU driver. Initiatives include bundling (e.g., Cordel + Kvalitetskontroll, ELinn + Elverdi), platform transitions to SmartCraft Spark, and expanding APIs to enable integrations across the suite. Pricing power is moderate: the company implements CPI-linked increases of 3–8%, but believes customers could bear higher rates given the clear ROI.

The company remains focused on SMEs rather than moving upmarket, though solutions do scale to larger enterprises (e.g., 18 of Finland’s top 20 contractors are customers). Strategy remains firmly anchored in digitizing the SME renovation and service segment.

SmartCraft competes less on price than on workflow fit and ROI. Customers pay roughly NOK 8 per user per day, or ~0.7% of wallet share, a small cost relative to recovered revenue and efficiency gains.

Large SaaS players have not penetrated the SME segment because it is fragmented, under-digitalized, and requires specialized, affordable tools rather than complex ERPs. SmartCraft’s moat lies in tailored workflows, sticky integrations, and regulatory compliance.

Integrations extend beyond ERP into wholesaler and distributor networks, as well as APIs with accounting platforms and national-level compliance systems. The new SmartCraft Spark platform is designed to unify solutions, reduce complexity, and accelerate cross-sell. Features like BIM support for Congrid and emissions data capture via Tellus further entrench its role in customer workflows.

Valuation is reasonable: ~25x FCF for a Rule of 50 company. One thing that is potentially a red flag is the operating deleverage in the model - margins have decreased from ~40% in 2022

SmartCraft Sophon Score

1. Market Opportunity (9/10)

Construction is one of Europe’s least digitalized industries, with 40–55% of SMEs still using pen-and-paper or spreadsheets. TAM is estimated at NOK 50 billion across the Nordics and U.K., ~700,000 firms, with penetration only 10–15%. Strong secular tailwinds (ESG, compliance, energy efficiency) add to demand. Large market, underpenetrated, long runway. Deduct 1 point because TAM expansion beyond Europe remains unproven.

2. Competitive Advantage (8/10)

SmartCraft has carved out a defensible niche in SME construction workflows. Its moat lies in tailored integrations (ERP, compliance, distributors), high workflow stickiness, and regulatory-driven adoption. Competition is fragmented; global SaaS giants focus on enterprise. Risk: workflows are not impossible to replicate, and there’s no single “cornered resource.”

3. Margins & Leverage (7/10)

Adjusted EBITDA margins hover ~37–40%, with SaaS-like unit economics. However, margin trend has dipped (41.6% in 2023 → 37.2% in 2024), showing some operating deleverage. Strong FCF conversion (~28% adj. EBITDA–CapEx margin) offsets this. Score reflects excellent profitability but recognizes margin pressure.

4. Reinvestment / Growth (8/10)

SmartCraft reinvests effectively: new modules (budgeting, Tellus), UK expansion, steady M&A, and platform unification (Spark). Organic ARR growth 6–10% plus bolt-ons. Medium-term target of 15–20% organic growth is credible given low digital penetration. Slight markdown since upsell/cross-sell is underdeveloped.

5. Business Model Quality (8/10)

Low capital intensity, SaaS gross margins, recurring-heavy revenue. Favorable working capital dynamics given prepaid subscriptions. Some dilution from acquired firms with low initial margins, but integration track record is strong.

6. Revenue Quality (9/10)

Recurring revenue is consistently >93% (95.5% in Q2 2025). Mission-critical workflows reduce churn, which mostly comes from bankruptcies among small firms. Large customers tend to downgrade, not leave. Cross-sell potential is high. This is textbook SaaS revenue quality.

7. Pricing & Unit Economics (8/10)

LTV/CAC was 18x in 2023 (down from >20x, still excellent). Payback short. Pricing power is moderate: 3–8% annual CPI-linked increases, but management undercharges relative to ROI (~NOK 8/user/day, <1% of wallet). Unit economics are strong; score reflects both efficiency and pricing headroom.

8. Competitive Dynamics (8/10)

Fragmented local competitors with limited scale; some consolidation but SmartCraft is positioned as category consolidator. Large global SaaS players (Procore, Autodesk) target enterprises, not SMEs. Competitive intensity is modest, though not zero. Risk is that as market matures, competition could increase.

9. Management (7/10)

Execution has been strong: disciplined M&A (12 deals since 2017), recurring revenue conversion, margin lift over time. Strategic clarity around SME focus. Deduction because cross-sell has lagged expectations and some operating deleverage suggests integration strain. No major governance red flags noted.

10. Financial Health (9/10)

Reasonable leverage, ample FCF to fund acquisitions, and capital-light SaaS model. No signs of balance sheet stress. Slight markdown as acquisitions create ongoing cash outlay needs.

Total Sophon Score: 81 / 100

Interpretation

SmartCraft scores very well as a durable compounder. Its strength lies in a massive underpenetrated TAM, SaaS-quality revenue, and sticky workflow integration. Weaknesses are modest: some operating deleverage, reliance on M&A to hit growth targets, and underexploited pricing power.

Overall, this is a high-quality software consolidator in an early-stage digitalization wave. At ~25x FCF, it is not optically cheap, but relative to its Rule of 50 profile (growth + margin), the valuation is fair. With ongoing market penetration and M&A optionality, upside seems credible.