Ucore Rare Metals (UURAF) Initiating Coverage

Emerging North American REE Processing Platform

Disclaimer: not financial advice

View: Buy

Sophon Score: 82/100 (see evaluation rubric at end of note)

Ucore Rare Metals sits at the nexus of strategic scarcity and technological disruption, offering Western markets a rare, non-Chinese source of critical rare earth elements. Its proprietary RapidSX platform and government-backed funding de-risk execution while positioning the company to capture outsized upside as demand for EVs, defense systems, and renewable energy grows. At ~3x EV/EBITDA potential versus peers and with a clear path to 12,000 tpa by 2027, the stock presents a highly asymmetric risk-reward profile with multi-bagger potential.

Ucore Rare Metals (UURAF) is positioning itself as a leading independent rare earth element (REE) processor in North America. The company is developing a proprietary processing technology (RapidSX) designed to address the sector’s structural bottleneck: the West’s near-total reliance on Chinese refining capacity. Ucore’s strategy centers on a demonstration facility in Ontario and a planned large-scale commercial complex in Louisiana, with first production targeted in 2026 and ramping to 12,000 tpa by 2027.

Relative to peers, we believe Ucore offers significant optionality as the U.S. seeks to localize REE processing. Based on peer multiples and conservative production assumptions, long-term valuation potential suggests material upside from current levels, though execution, financing, and scale remain key risks.

Supply Concentration: China currently accounts for ~60% of global REE mining but ~95% of downstream refining/processing capacity. This imbalance has created strategic vulnerabilities for Western supply chains, particularly for defense, EV, and high-tech applications.

Strategic Importance: Rare earths are essential for a wide range of applications including EV motors, wind turbines, defense systems, MRIs, and consumer electronics. Access to refined REEs is critical for the U.S. and its allies in maintaining industrial and national security competitiveness.

Bottleneck Economics: While upstream mining has drawn significant investor interest (MP Materials), processing capacity is the current constraint. Control of this step in the value chain is viewed as a strategic lever, analogous to oil refining’s importance during the early petroleum industry buildout.

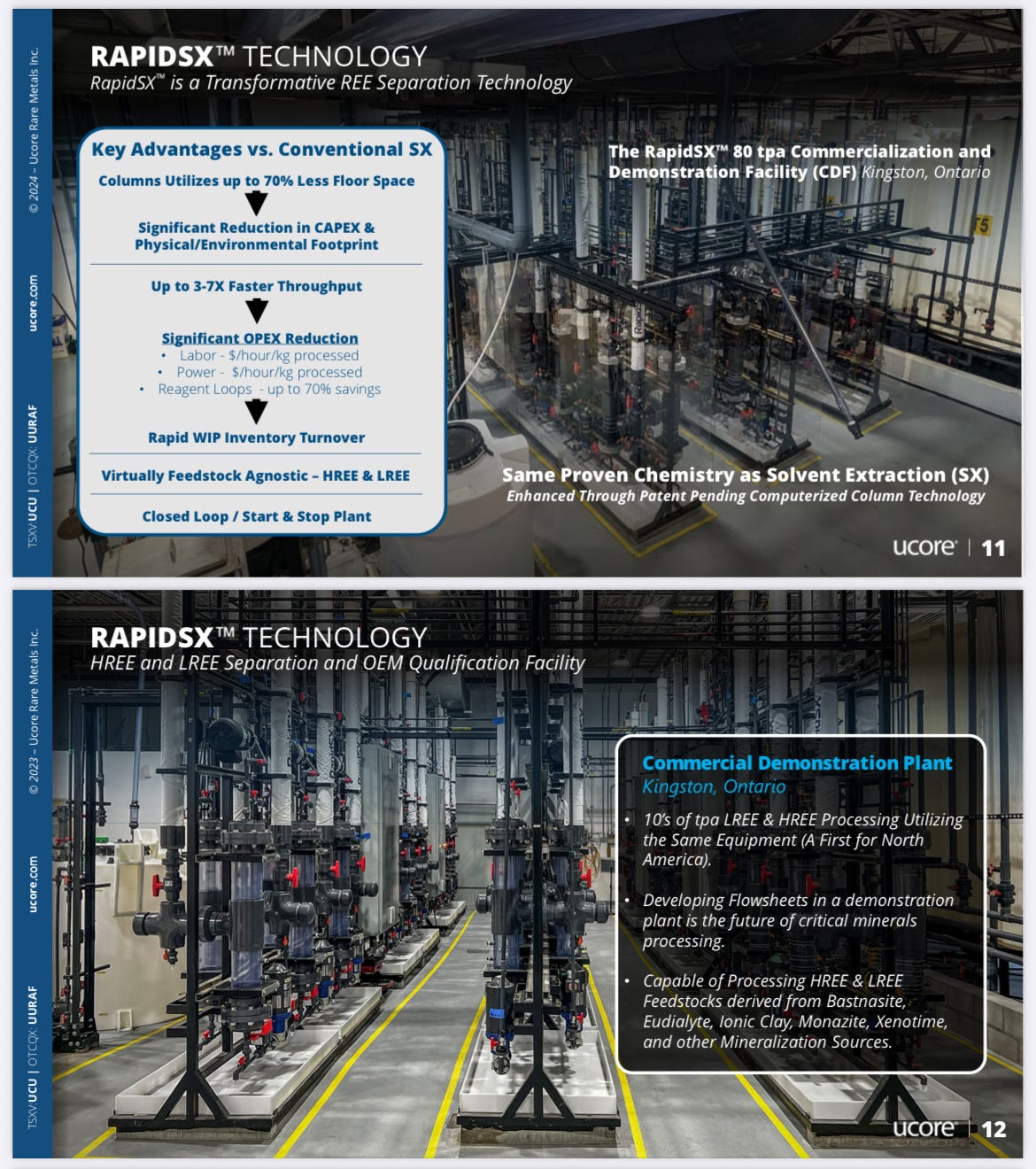

Technology Platform (RapidSX)

Modular, automated solvent-extraction platform designed to improve throughput by up to 10x relative to conventional systems.

Capable of processing both light and heavy REEs, with adaptability across feedstocks.

Proprietary IP secured via the acquisition of Innovation Metals Corp.

Facilities

Ontario Demo Plant: Proof-of-concept site currently validating RapidSX efficiency. The facility is able to operate at commercial-like conditions with minimal staffing due to high levels of automation.

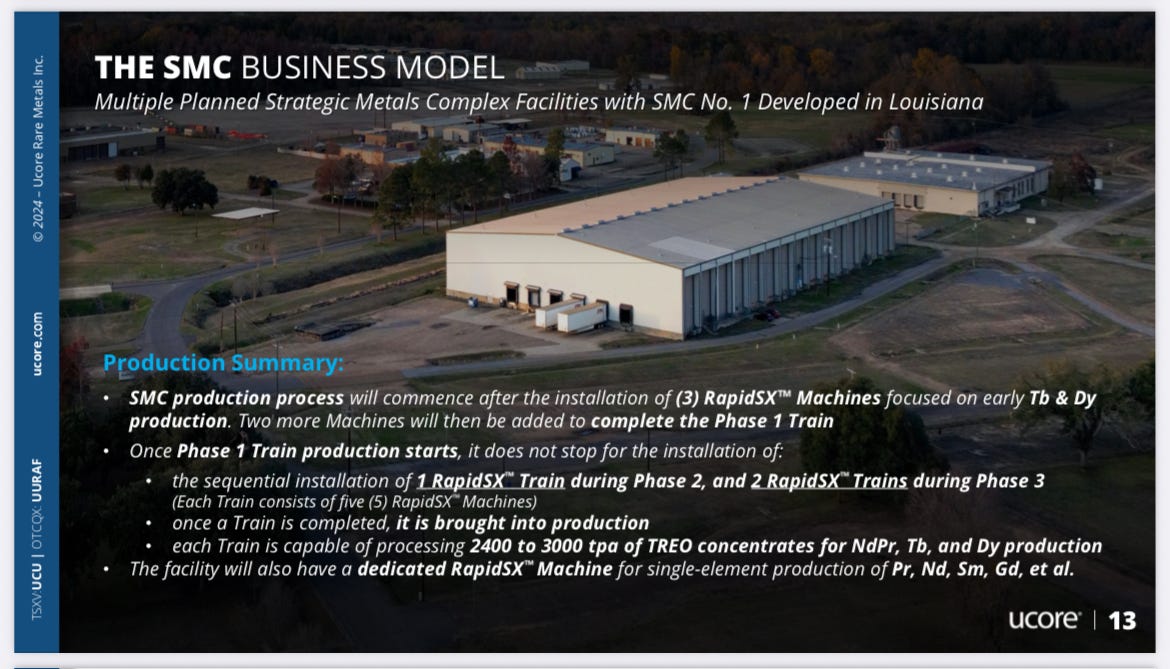

Louisiana Strategic Metals Complex (SMC): Planned commercial-scale refinery with 12,000 tpa nameplate capacity (post-ramp). Site benefits include Foreign Trade Zone designation, brownfield infrastructure, and ~$22mn in DoD grants. Initial 3,000 tpa line expected May 2026.

Management

CEO Pat Ryan: >25 years of experience in supply chain management and EV-related industries.

CFO Peter Manuel: Extensive governance and financial oversight background, >17 years in resource-sector advisory.

Financial Overview:

Capex: Louisiana facility estimated at ~$65mn initial build cost; >50% already funded through grants and existing financing.

Stage 1 operations (~2,500 tpa TREO) could generate ~$150mn in revenue at steady state.

At 12–15% EBITDA margins initially, ~$20mn EBITDA is achievable in early operations; scalability to 25–30% EBITDA margins at full ramp (~10,000 tpa) suggests potential for ~$200mn run-rate EBITDA by 2027.

Additional ~$100mn required to complete full three-line Louisiana buildout. Potential funding sources include equity, strategic partners, offtake agreements, and further U.S. government support.

Valuation:

Peer Comparison (MP Materials):

MP Materials (market cap ~$11bn) trades at ~39x 2026e EBITDA and 26x 2027e EBITDA.

MP targets larger-scale light REE production but does not focus on heavy REEs, which are more challenging to process and often command higher premiums.

Scenario Analysis:

At full 2027 ramp ($200mn EBITDA potential), applying MP’s current EBITDA multiple (27x) implies a multi-billion-dollar enterprise valuation for Ucore.

Even applying material discounts, Ucore’s implied valuation at scale suggests meaningful upside from today’s ~$220mn EV.

Catalysts:

U.S. market uplisting (potential rerating event).

Progress updates on Louisiana SMC construction (initial 2026 startup).

Additional government or strategic funding announcements.

Expanded offtake agreements.

Initiation of sell-side coverage as project de-risks.

Risks:

Construction and permitting delays at Louisiana SMC.

Capital raising requirements and dilution.

Technology scale-up risk for RapidSX.

Competitive response from incumbents (e.g., MP Materials).

Commodity price volatility for REEs.

Ucore is an early-stage but strategically well-positioned entrant in Western REE processing. While execution and financing remain key hurdles, the company’s proprietary technology, U.S.-backed funding support, and focus on heavy REEs present an asymmetric profile relative to current valuation.

Sophon Score Breakdown

Market Opportunity – 10/10

Ucore is targeting the North American rare earth processing market, a strategically critical and rapidly growing sector. Global demand for REEs is expected to expand due to EVs, wind turbines, defense systems, and electronics. Western reliance on Chinese refining (~95% of capacity) creates a large TAM for a local processor.

Competitive Advantage – 10/10

Proprietary RapidSX technology provides up to 10x throughput improvement and handles both light and heavy REEs. Early-stage IP and first-mover advantage in North America give defensibility, though competitors may emerge as the sector grows. Government support (grants, trade-zone benefits) reinforces positioning.

Margins & Leverage – 6/10

Early-stage operations will have modest margins (12–15% EBITDA initially), with potential to reach 25–30% at full ramp. Capital intensity is moderate (~$65M for Louisiana facility), with partial funding from grants. Leverage risk exists during scale-up and funding of full three-line complex.

Reinvestment / Growth – 9/10

Strong growth optionality: ramping from demonstration plant to full-scale Louisiana SMC (12,000 tpa by 2027) enables significant EBITDA expansion. Additional upside from strategic partnerships, government funding, and offtake agreements. Proprietary tech supports incremental capacity expansion.

Business Model Quality – 7/10

Processing-focused, modular, and automated platform reduces staffing requirements and allows scalable operations. Model is capital-intensive relative to software/consumer businesses but less risky than pure exploration/mining upstream.

Revenue Quality – 6/10

Future revenue is predictable once operations commence, but the company is pre-revenue at scale. EBITDA depends on successful construction, ramp, and product offtake. Revenue quality improves as operations stabilize.

Pricing & Unit Economics – 7/10

Heavy REEs are high-value, commanding premiums relative to light REEs. Modular processing technology reduces per-unit costs, supporting strong unit economics at scale. Early-stage ramp may have some inefficiencies.

Competitive Dynamics – 10/10

Western supply chain constraints and U.S. government interest create structural tailwinds. Early entry into North American heavy REE processing is strategically advantageous. Competitive response from incumbents (e.g., MP Materials) is possible but mitigated by first-mover tech advantage.

Management – 10/10

CEO and CFO bring extensive operational and resource-sector experience. Strategic alignment with government objectives improves credibility, though execution risk is meaningful given early-stage nature of facilities.

Financial Health – 7/10

Partially funded Louisiana build (~50% via grants/existing financing) and CAD/US cash provides runway, but ~$100M additional capital needed. Zero operational revenue currently; balance sheet risk tied to construction, scale-up, and funding.

Total Sophon Score: 82 / 100

Ucore screens as a high-potential, early-stage strategic play with asymmetric upside, primarily driven by proprietary processing technology, Western REE supply constraints, and government support. Execution and financing risks are material, but the upside from first-mover advantage in a critical market is significant.